The Basics

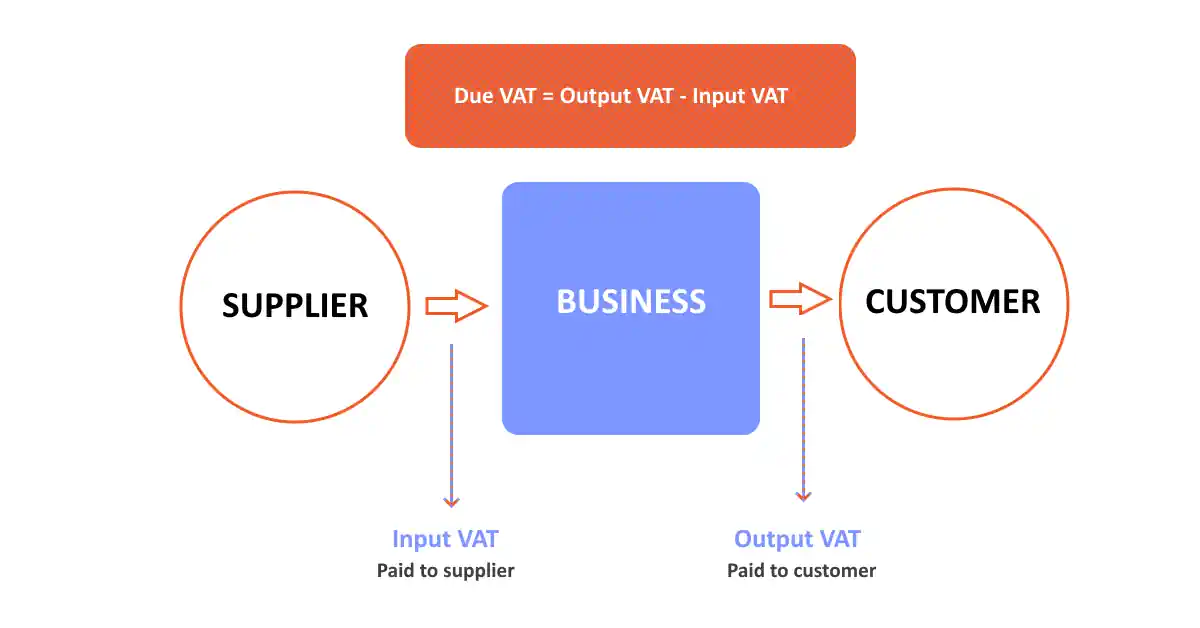

Broadly speaking, businesses do not suffer the burden of VAT, but the final consumer does. However, sellers are responsible for collecting it and remitting it to the Tax Administration of Montenegro. At every point in the supply chain where value is added to a product or service, each supplier, business, or customer is charged VAT on taxable supplies delivered to them, given that they are provided by a VAT-registered supplier.

As a consequence, businesses can reclaim Input Value-Added Tax paid on purchases for standard-, reduced-, and zero-rated supplies, which reduces their costs and increases profits. Businesses that are not able to recover Input VAT, however, do face an additional cost. To understand how Value-Added Tax works in practice, see the example below:

Example

A manufacturer sells a kitchen to a wholesaler for 10.000,00€ and charges him Value-Added Tax (VAT) at Montenegro’s standard rate of 21%. The kitchen manufacturer then transfers the amount that is due for VAT – 2.100,00€ – to the tax authorities when submitting the mandatory monthly VAT return.

The wholesaler then sells the kitchen to a retailer for 20.000,00€ plus 21% VAT, for a total of 24.200,00€. The (VAT-registered) wholesaler is also obliged to file a monthly VAT return, and must pay Output VAT of 4.200,00€ on the kitchen. He can offset the 2.100,00€ already paid to the manufacturer as Input VAT, leaving 2.100,00€ to remit to the Tax Administration of Montenegro.

When a customer buys the kitchen from the retailer, VAT must be added to the selling price. The retailer sells the kitchen for 30.000,00€, plus 21% VAT, resulting in a total price of 36.300,00€ for the customer. The retailer’s net VAT (Output VAT of 6.300,00€ minus Input VAT of 4.200,00€) results in a payment of 2.100,00€ to the tax authorities.

Montenegro’s tax authorities have thus received 21% of the price paid by the consumer for the kitchen, amounting to 6.300,00€. The kitchen manufacturer, wholesaler, and retailer each only remitted the VAT they charged to the next buyer in the supply chain.

VAT Refunds

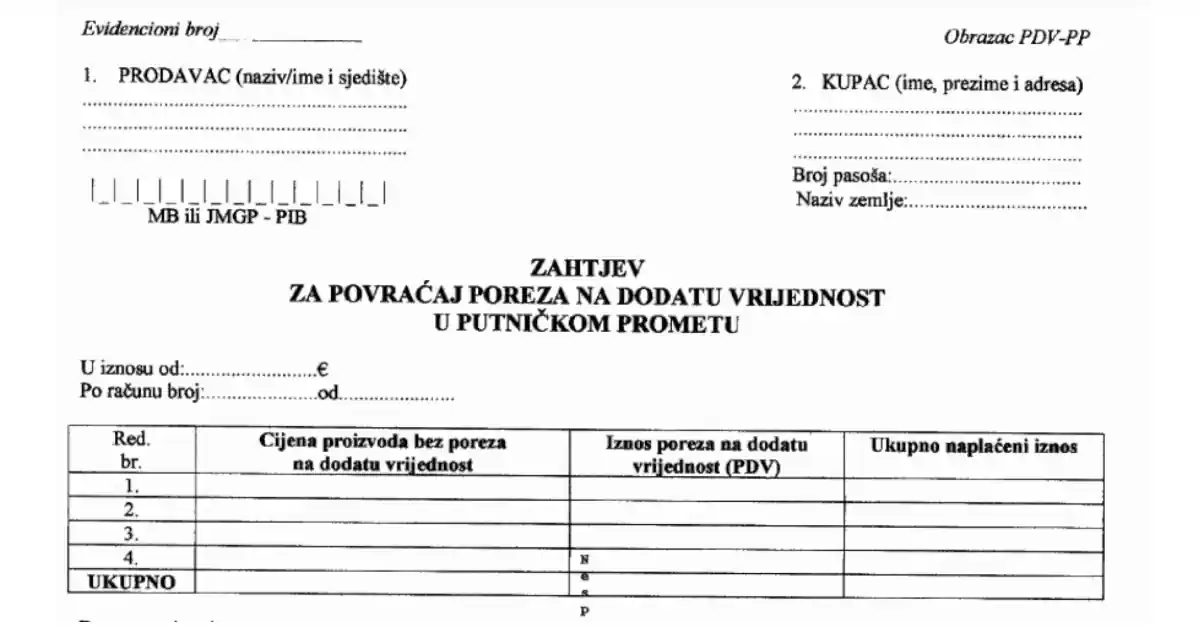

Non-residents of Montenegro may claim a VAT refund on goods purchased during their trip, provided the goods are presented to customs upon departure within three months of purchase. You must also present the original invoice along with the ‘PDV-PP’ VAT refund form, which must be completed and signed/stamped by the vendor.

Here are some additional points to consider:

- The invoice value must be at least 100,00€

- No VAT refund is available for alcoholic beverages, tobacco products, or mineral fuels

- Spare parts for cars and vessels installed in Montenegro are eligible for a refund

- The claim must be validated by Montenegro’s customs authority before you leave the country

The certified ‘PDV-PP’ form must then be sent or returned to the vendor within six months of purchase, so they can process the VAT refund, either in cash or via wire transfer